All Categories

Featured

Table of Contents

For most individuals, the biggest problem with the unlimited banking idea is that preliminary hit to very early liquidity caused by the prices. Although this disadvantage of limitless banking can be reduced considerably with correct plan design, the first years will constantly be the worst years with any type of Whole Life plan.

That stated, there are particular boundless financial life insurance coverage policies made mainly for high very early money worth (HECV) of over 90% in the very first year. Nonetheless, the long-lasting performance will often significantly lag the best-performing Infinite Financial life insurance policy policies. Having accessibility to that additional four figures in the very first couple of years might come at the cost of 6-figures down the roadway.

You in fact obtain some considerable lasting advantages that help you recover these early costs and then some. We locate that this prevented very early liquidity trouble with limitless banking is extra psychological than anything else once thoroughly checked out. Actually, if they absolutely needed every dime of the cash missing out on from their boundless banking life insurance coverage plan in the initial couple of years.

Tag: infinite banking idea In this episode, I speak about funds with Mary Jo Irmen that shows the Infinite Financial Idea. With the increase of TikTok as an information-sharing platform, monetary suggestions and techniques have actually discovered an unique way of dispersing. One such strategy that has been making the rounds is the infinite financial idea, or IBC for short, garnering recommendations from celebrities like rap artist Waka Flocka Fire.

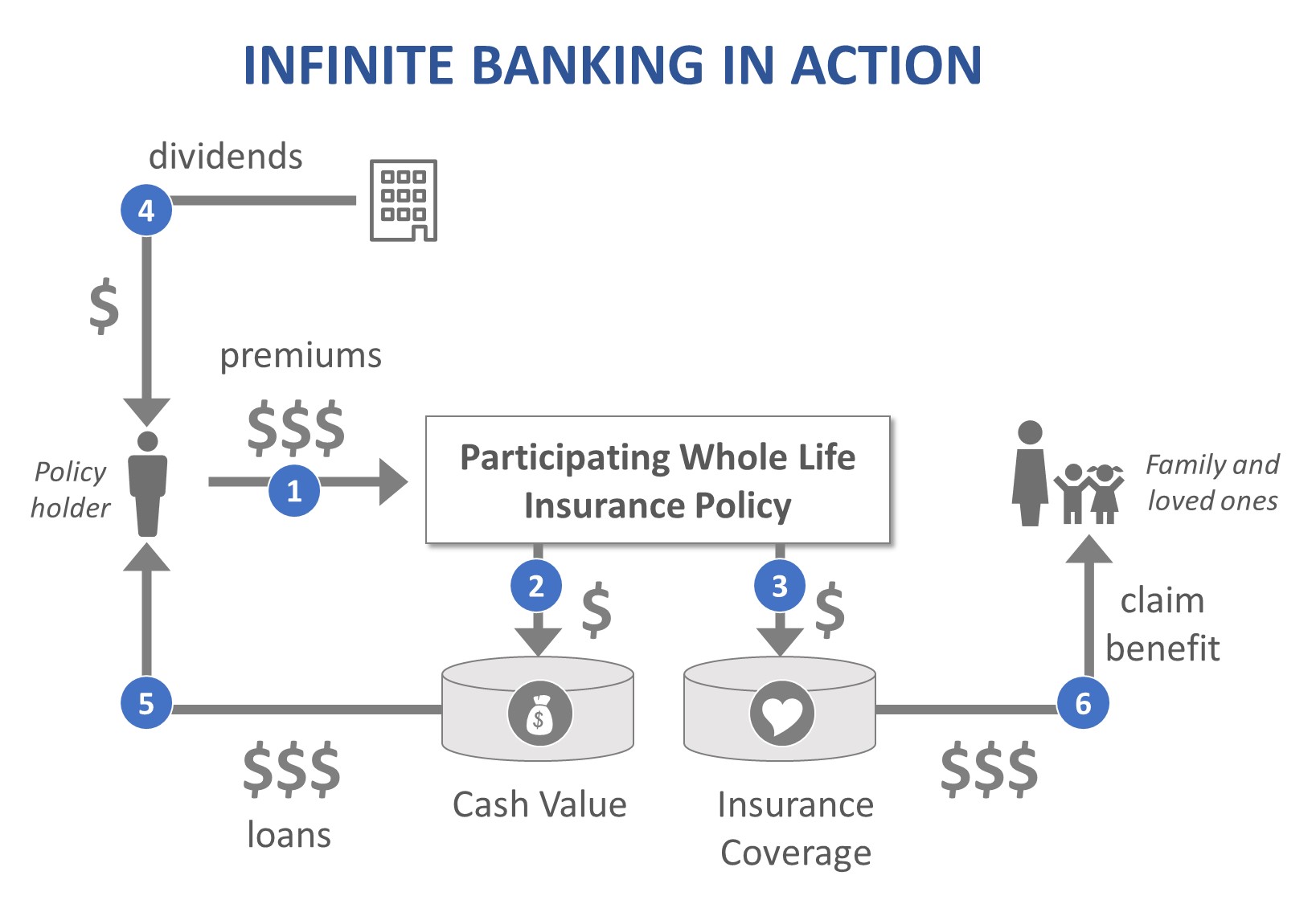

Within these plans, the cash value expands based on a price set by the insurance company. Once a significant cash money worth accumulates, policyholders can acquire a money worth loan. These finances vary from traditional ones, with life insurance policy working as collateral, implying one could shed their protection if borrowing excessively without adequate money value to support the insurance expenses.

And while the allure of these policies appears, there are natural limitations and dangers, necessitating thorough cash value tracking. The method's authenticity isn't black and white. For high-net-worth people or company owner, particularly those making use of techniques like company-owned life insurance (COLI), the advantages of tax breaks and substance growth could be appealing.

Infinite Bank

The appeal of boundless financial does not negate its challenges: Expense: The foundational requirement, a permanent life insurance policy policy, is costlier than its term counterparts. Eligibility: Not every person gets approved for whole life insurance policy as a result of strenuous underwriting procedures that can leave out those with details health and wellness or way of life conditions. Intricacy and danger: The complex nature of IBC, paired with its risks, may hinder many, especially when less complex and much less high-risk options are readily available.

Assigning around 10% of your monthly revenue to the plan is simply not possible for the majority of people. Part of what you review below is simply a reiteration of what has already been said above.

So prior to you obtain on your own into a scenario you're not planned for, recognize the adhering to initially: Although the principle is frequently offered thus, you're not really taking a car loan from on your own. If that were the situation, you would not have to settle it. Instead, you're borrowing from the insurer and have to repay it with passion.

Some social networks articles suggest utilizing cash value from whole life insurance policy to pay for bank card financial obligation. The idea is that when you pay back the car loan with rate of interest, the quantity will certainly be returned to your investments. That's not exactly how it works. When you repay the finance, a portion of that passion mosts likely to the insurance provider.

For the first numerous years, you'll be repaying the commission. This makes it extremely challenging for your policy to accumulate value throughout this moment. Whole life insurance policy expenses 5 to 15 times much more than term insurance. Lots of people simply can't afford it. Unless you can pay for to pay a couple of to a number of hundred dollars for the following decade or more, IBC won't work for you.

Does Infinite Banking Work

If you call for life insurance, right here are some valuable suggestions to take into consideration: Think about term life insurance policy. Make certain to shop about for the finest rate.

Copyright (c) 2023, Intercom, Inc. () with Booked Font Style Call "Montserrat". Copyright (c) 2023, Intercom, Inc. (legal@intercom.io) with Scheduled Font Name "Montserrat".

Cut Bank Schools Infinite Campus

As a certified public accountant specializing in genuine estate investing, I have actually combed shoulders with the "Infinite Financial Idea" (IBC) much more times than I can count. I have actually even interviewed professionals on the topic. The main draw, in addition to the noticeable life insurance policy advantages, was always the concept of developing cash money worth within a permanent life insurance coverage plan and borrowing against it.

Certain, that makes good sense. Honestly, I constantly assumed that cash would be much better invested directly on investments instead than channeling it via a life insurance coverage plan Up until I discovered exactly how IBC might be incorporated with an Irrevocable Life Insurance Depend On (ILIT) to produce generational wide range. Allow's start with the basics.

Infinite Income System

When you borrow versus your policy's cash value, there's no collection repayment timetable, offering you the liberty to handle the finance on your terms. The money value proceeds to expand based on the policy's guarantees and returns. This setup enables you to accessibility liquidity without disrupting the lasting development of your plan, offered that the financing and rate of interest are handled intelligently.

The process proceeds with future generations. As grandchildren are born and mature, the ILIT can purchase life insurance plans on their lives also. The trust then builds up several plans, each with expanding money values and death benefits. With these policies in place, the ILIT successfully becomes a "Household Financial institution." Family participants can take fundings from the ILIT, using the money value of the plans to fund investments, start services, or cover major expenditures.

An important element of managing this Family members Bank is using the HEMS requirement, which represents "Health and wellness, Education, Upkeep, or Support." This guideline is typically included in depend on contracts to route the trustee on how they can distribute funds to recipients. By sticking to the HEMS standard, the trust fund ensures that circulations are made for vital demands and long-term support, protecting the count on's assets while still providing for relative.

Enhanced Flexibility: Unlike rigid small business loan, you regulate the payment terms when obtaining from your own plan. This enables you to structure repayments in such a way that lines up with your service money flow. r nelson nash net worth. Improved Cash Flow: By financing overhead through policy loans, you can potentially liberate cash that would otherwise be connected up in standard financing payments or equipment leases

He has the exact same tools, but has additionally developed added cash value in his plan and received tax obligation advantages. Plus, he now has $50,000 readily available in his plan to make use of for future chances or expenditures. In spite of its possible advantages, some individuals remain unconvinced of the Infinite Banking Principle. Allow's resolve a couple of typical concerns: "Isn't this simply costly life insurance policy?" While it's real that the premiums for an effectively structured entire life policy may be greater than term insurance coverage, it is essential to see it as more than simply life insurance.

Infinite Banking Concept Dave Ramsey

It has to do with producing a versatile financing system that provides you control and provides multiple advantages. When used tactically, it can enhance other financial investments and company techniques. If you're captivated by the capacity of the Infinite Financial Concept for your company, here are some steps to take into consideration: Enlighten Yourself: Dive much deeper into the idea through trustworthy books, workshops, or examinations with experienced experts.

{kind=link}

Latest Posts

Become Your Own Banker Whole Life Insurance

Infinite Banking System Review

Cipher Bioshock Infinite Bank